Trying to decide between a single-family home, condo, or townhome in San Mateo County? There is no one-size-fits-all answer. Each option has strengths, tradeoffs, and a different fit depending on your budget, lifestyle, and tolerance for shared decision-making.

Condos can absolutely make sense. For many buyers, they are the most realistic path to homeownership on the Peninsula. But if you are going to buy one, it helps to go in with your eyes open. There are some downsides that do not always show up in the glossy listing photos or the marketing package.

After many years helping buyers and sellers across San Mateo County, we have seen the good, the bad, and the annoying when it comes to condo living. Some issues are minor inconveniences. Others can seriously affect resale value, financing, monthly costs, or your quality of life.

This guide walks through eight reasons to be cautious before buying a condo, along with real-world examples and what to pay attention to before you commit.

Table of Contents

- 1. Privacy and natural light

- 2. HOA drama and shared decision making

- 3. Low HOA fees can be a red flag

- 4. Property condition and building risk

- 5. Rental restrictions can limit your options

- 6. Insurance is getting harder and more expensive

- 7. Mismanagement does happen

- 8. Condos often appreciate more slowly than houses

- How to buy a condo the smart way

- FAQ

1. Privacy and natural light

The most obvious downside of condo living is also one of the most important. In most condo buildings, you are sharing walls, floors, ceilings, hallways, and common areas with other people. That means less privacy, more noise, and sometimes a lot more sensory overlap than buyers expect.

If you are in an older building or one with weaker sound insulation, you may hear neighbors walking around, coughing, sneezing, moving furniture, or running a blender. If windows are open, sounds carry even more. Smells do too. You may catch whatever someone nearby is cooking, and not always at the ideal time.

We have even seen situations where the location of the unit itself became the deciding factor. In one condo complex in Woodlake in San Mateo, which is actually a very desirable complex on the Peninsula, a unit near a restaurant had noticeable food aromas drifting onto the balcony. It was not terrible, but it was enough for the buyer to pass.

Natural light is another factor that gets overlooked. A house usually has windows on all sides. A condo often does not. Shared walls can limit your exposure, and interior-facing units or units boxed in by neighboring buildings can feel darker than expected.

If you are considering a condo, a corner unit with good sun exposure is worth a serious premium. The difference in livability can be substantial.

2. HOA drama and shared decision making

When you buy a condo, you are not just buying real estate. You are also buying into a system of governance. That system is the homeowners association, or HOA, and it can be either functional and boring or frustrating and exhausting.

Most HOA boards are made up of volunteer owners. That does not mean they are bad people. Usually they are trying their best. But they often do not have professional property management experience, construction expertise, financial training, or the time needed to make ideal decisions. Even when a complex has professional management, the board still has to approve major decisions, budgets, repairs, and policies.

And unlike owning a house, you do not just decide what to do and move on. In an HOA, everything requires some level of consensus. That means meetings, disagreements, politics, delays, and compromise.

We have seen relatively simple ideas turn into building-wide drama. One seller in an older building wanted to refresh the lobby because it looked dated and smelled old. His thinking was reasonable: nicer common areas help units show better and may support higher sale prices. Instead, the discussion became so heated that one board member said he would never speak to him again and eventually sold his own unit to leave the building.

That is an extreme example, but shared living makes conflict more likely. If you want maximum autonomy, condos may feel restrictive.

3. Low HOA fees can be a red flag

A lot of buyers get excited when they see very low HOA dues. On the surface, that makes sense. Lower monthly payments sound great. But low dues are not automatically a sign of a healthy association. In some cases, they are the opposite.

HOA dues generally cover two big buckets:

- Operating expenses such as landscaping, lighting, insurance, and routine maintenance

- Reserve contributions for future major repairs and replacement projects

If dues are artificially low, the HOA may not be putting enough money into reserves. That becomes a problem when expensive work comes up, which it always does. Roofs wear out. Siding fails. Windows need replacement. Plumbing, decks, elevators, and common areas all age.

If the reserves are weak and the association does not have enough cash on hand, owners can get hit with a special assessment. That means everyone has to write a check, often based on the size of their unit, to cover the shortfall.

Those assessments are not pocket change. Depending on the project, they might be $5,000, $20,000, $30,000, or more.

Also, keep in mind that HOA dues rarely stay flat forever. Insurance, labor, utilities, and maintenance costs rise over time. So if you are analyzing affordability, do not assume today’s dues are permanent.

4. Property condition and building risk

With a condo, your home is tied to the condition of the entire building. Even if your individual unit is beautifully remodeled, problems in the structure, exterior, or common systems can still hurt you.

At the most serious end of the spectrum, poor maintenance can become a safety issue. The condo collapse in Surfside, Florida in 2021 is a tragic reminder of what can happen when warning signs are missed or deferred too long. That event understandably changed how many buyers think about condo buildings and deferred maintenance.

There is another issue that comes up more often in newer California developments: construction defect litigation. Modern construction is complicated, and in the first several years after a project is completed, problems can surface that should not have happened. In California, HOAs generally have a ten-year window after first occupancy to pursue claims against a developer or builder for defects.

Sometimes those claims are legitimate and serious. But if you are trying to sell during active litigation, you may run into a huge problem: many lenders will not finance a condo or townhome if there is pending litigation in the HOA.

That wipes out a large portion of the buyer pool. Suddenly, the likely buyers are cash buyers only, and cash buyers usually expect a discount.

We have seen this happen in San Mateo. In one case at 1700 De Anza, pending litigation essentially crushed the resale market at the time. A cash buyer ended up getting an excellent deal because financing options were so limited for everyone else.

5. Rental restrictions can limit your options

One of the less obvious risks of condo ownership is that your future plans may not line up with HOA rules.

Many condo associations cap the percentage of units that can be rented out. The idea is that owner-occupied buildings may be better maintained or more stable. Whether that is always true is debatable, especially in San Mateo County, but the rules are common.

The problem is what happens when your life changes.

Maybe you buy a condo when you are single. Then you get married. Then you have a child and need more space. Or maybe you get transferred for work and want to hold the property as a rental. If the building has already hit its rental cap, you may not be able to lease your unit even if keeping it would be the smartest financial move.

We saw this with an owner on Elm Street in San Mateo. He bought a nice condo early in life, later married, and eventually needed a larger home in Burlingame after starting a family. He wanted to keep the condo and rent it out as passive income. He did not need to sell in order to buy the next home.

But the HOA had already reached its rental maximum, around 30 percent of the building. He was effectively forced to sell instead.

Unfortunately, the timing was bad and the market had declined. He ended up selling for dramatically less than what similar units in the building had sold for several years earlier. That low sale also likely hurt values for other owners because it became a comparable sale on the record.

Before buying a condo, always ask: If our plans change, can we rent this out? You do not want to discover the answer when you no longer have flexibility.

6. Insurance is getting harder and more expensive

California insurance has become a much bigger issue over the past year, and condo owners are not immune. Insurers are repricing risk, especially around natural hazards and aging properties, and that has pushed premiums up significantly.

For condos, this can show up in several ways.

- The HOA’s master policy may get more expensive, which can lead to higher dues

- Older buildings with deferred maintenance may face tougher underwriting scrutiny

- Insurers may require inspections or upgrades before renewing coverage

- Earthquake insurance is often absent entirely

That last point matters in the Bay Area. If earthquake coverage is important to you, you should know that it is very uncommon for an HOA to carry it. The coverage is expensive, and getting a majority of owners to vote in favor of paying for it is usually difficult. Across many years of transactions, we have only seen a couple of HOAs that actually had earthquake insurance in place.

So when evaluating a condo, do not just ask whether the building is insured. Ask how well it is insured, what the master policy covers, and what major risks may still fall back on owners.

7. Mismanagement does happen

Most HOAs are not disasters. Plenty are run responsibly. But because they are handling real money, major repair decisions, legal obligations, and contractor relationships, things can go sideways.

Mismanagement does not always mean fraud. Sometimes it is simply poor judgment. Maybe the board did not get competitive bids. Maybe money was spent on unnecessary consultants or projects. Maybe reserves were not built properly. Maybe the books looked clean on paper while deeper issues were being ignored.

And yes, in rare cases, outright theft can happen.

One San Mateo complex with nearly a thousand units reportedly had an employee in finance embezzle more than $2.8 million over a seven-year period. That is staggering. It raises all kinds of uncomfortable questions about oversight, auditing, and who was actually checking the flow of money.

This is not typical, but it is a reminder that buyers should not treat HOA financials as background noise. They matter.

If you are buying into an HOA, do your due diligence before you write an offer whenever possible. Read the documents. Read the CC&Rs. Read the meeting minutes. Review the insurance information. Walk the property at different times of day. Get a feel for how the place is maintained and how the community operates.

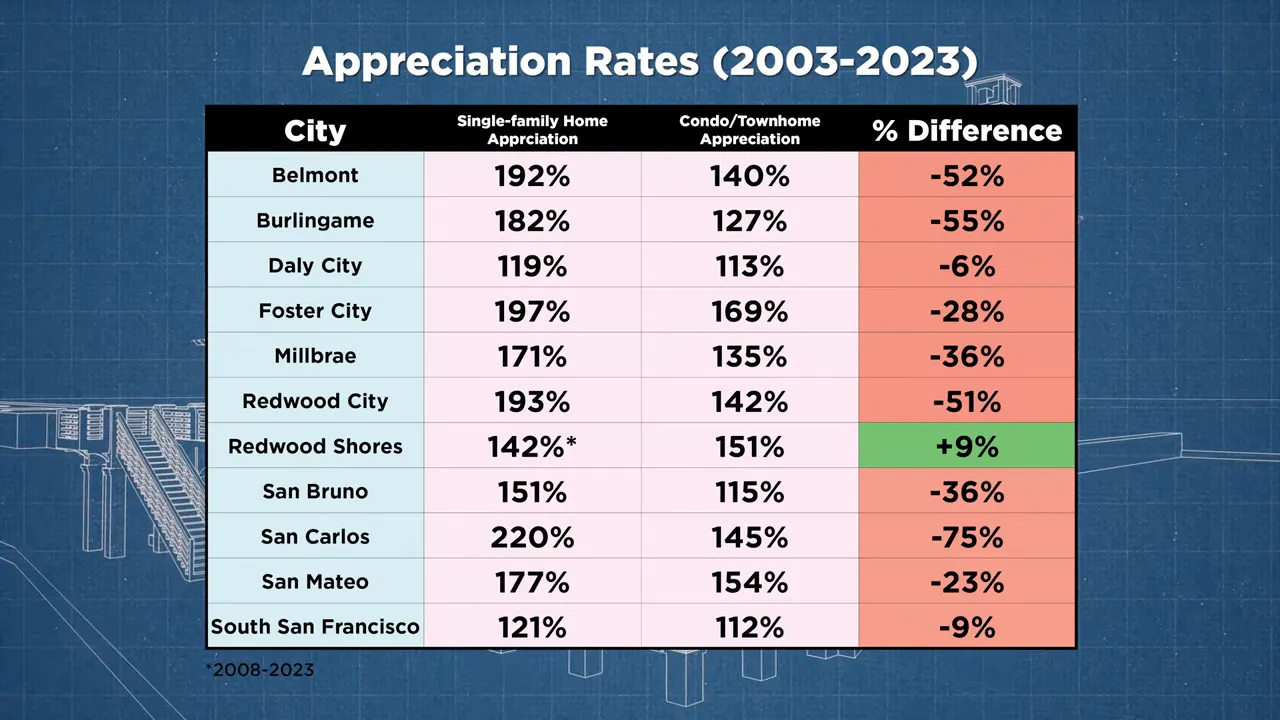

8. Condos often appreciate more slowly than houses

Here is the biggest long-term reason many buyers still prefer single-family homes when they can afford them: appreciation.

Over a 20-year period in San Mateo County, homes outperformed condos and townhomes in rate of appreciation. That should not be especially shocking. The market is telling us that, on balance, more buyers around here prefer a house without an HOA if they can make the numbers work.

That does not mean buying a condo is a bad move. Not at all. A condo can still be a fantastic first step into Peninsula real estate, and for many people it is the only practical step without stretching finances to an unhealthy level.

But if you are comparing property types strictly from an investment angle, you should understand that condos often come with slower appreciation than detached homes. The lower entry price is the tradeoff.

That is why the condo decision should be framed honestly. You may not get the same upside as a house, but you may also avoid having to spend hundreds of thousands or even millions more upfront to get into the market.

How to buy a condo the smart way

After all of that, buying a condo may sound a little grim. It should not. Plenty of people buy condos and townhomes in San Mateo County and are very happy. The key is not avoiding condos entirely. The key is buying the right condo in the right building for the right reasons.

Here are the basics we would focus on before moving forward:

- Study the HOA documents. Look closely at reserves, meeting minutes, rules, insurance, and any mention of litigation or major repair needs.

- Evaluate the building, not just the unit. A nice kitchen does not offset poor exterior maintenance or weak association finances.

- Ask about rental policies. Future flexibility matters more than many buyers realize.

- Understand the true monthly cost. That includes dues today and the possibility of increases or assessments later.

- Pay attention to livability. Noise, light, privacy, location within the complex, and proximity to restaurants or roads can all affect daily life.

- Think about resale from day one. The same things that matter to you will matter to future buyers.

If you buy with your eyes open and do your homework, condos can still be an excellent option. But they are not interchangeable with houses, and they are not automatically easier just because the price tag is lower.

In San Mateo County especially, where housing costs are high and every decision has tradeoffs, understanding those distinctions can save you from expensive surprises later.

Want to buy a condo in San Mateo County without running into expensive surprises? I can help you analyze the HOA documents, understand real monthly costs (including dues increases and reserves), and compare buildings with your long-term goals in mind. Call or text me at 650-822-7088 to get started.

FAQ

Is buying a condo in San Mateo County always a bad idea?

No. Condos can be a smart entry point into homeownership, especially on the Peninsula where single-family homes are much more expensive. The point is not that condos are bad. The point is that buyers should understand the tradeoffs before buying.

What is the biggest risk when buying a condo?

There is no single risk for every buyer, but HOA health is a major one. Weak reserves, poor maintenance, litigation, insurance issues, or bad management can affect your monthly cost, resale value, and overall ownership experience.

Are low HOA dues a good sign?

Not necessarily. Low dues can look attractive, but they may also mean the HOA is underfunding reserves. That can lead to special assessments later when expensive repairs come up.

Can an HOA stop me from renting out my condo?

Yes. Some HOAs cap the number of units that can be rented. If the building is already at its limit, you may not be allowed to lease your unit even if your personal situation changes.

Do condo buildings usually have earthquake insurance in California?

Usually not. Earthquake insurance for HOAs is often very expensive, and many associations do not carry it. If this matters to you, it is worth confirming early in the process.

Do condos appreciate less than single-family homes in San Mateo County?

Over the long term, homes have generally appreciated faster than condos and townhomes in San Mateo County. That said, condos can still appreciate and may still be the right choice depending on budget and goals.

What documents should I review before buying a condo?

Focus on the CC&Rs, HOA meeting minutes, reserve information, insurance details, and any disclosures related to repairs, deferred maintenance, or litigation. Those documents can reveal a lot about how the building is run.

Read More: 6 San Mateo Neighborhoods Where You Can Still Buy a 3-Bedroom Home Under $2.5M